It's a question almost everyone faces, from seasoned spenders to those just getting started with their finances. On the surface, they look so similar – plastic rectangles with numbers, used for payments. But beneath that shiny exterior lies a world of difference that can profoundly impact your financial health.

Deciding which is smarter to use: credit card or debit card isn't about declaring one an absolute winner. It's about understanding their distinct mechanisms, their strengths, and their weaknesses. It's about knowing when each card becomes your best financial ally and when it might lead you down a tricky path. This isn't just about convenience; it's about smart financial planning with credit and debit cards, protecting your money, and building a secure future.

As an expert who's seen the financial triumphs and pitfalls associated with both, I can tell you that mastery of these two tools is a cornerstone of effective personal finance. This guide will deep dive into the difference between credit and debit card, unravel their credit card advantages and disadvantages versus debit card pros and cons, and give you the knowledge to confidently choose the right plastic for every situation. By the end, you'll not only know which is safer: credit or debit card but also how to leverage each for your financial benefit.

1. What’s the main difference between a credit card and a debit card?

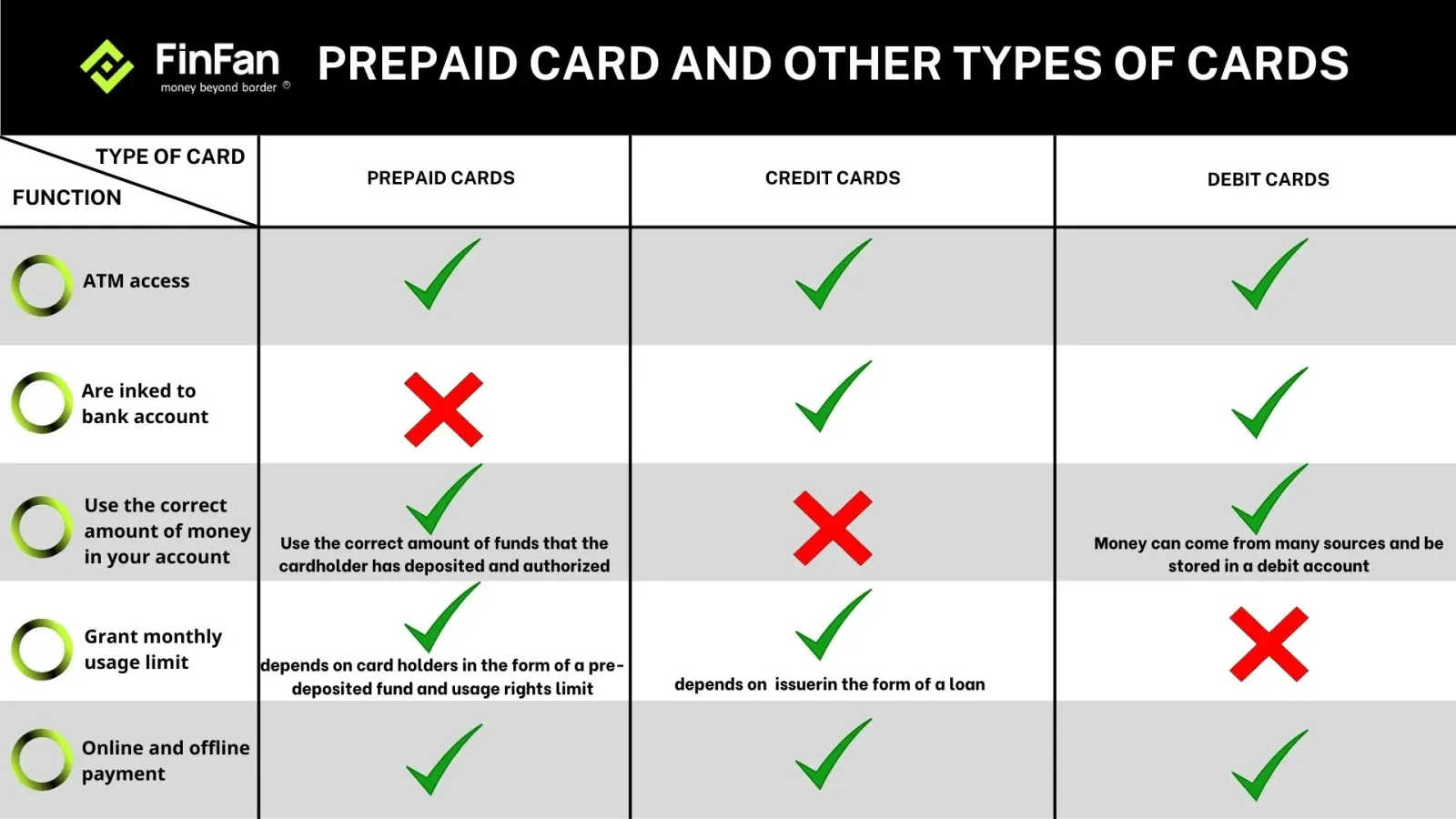

At their core, the main difference between a credit card and a debit card boils down to one fundamental principle: where the money comes from when you make a purchase. This distinction dictates nearly every other aspect of how these cards function and their impact on your finances.

Debit Card: Your Money, Direct from Your Bank Account

Think of a debit card as an electronic key to your checking account. When you use a debit card:

-

Source of Funds: The money for your purchase is immediately, or very nearly immediately, deducted directly from your checking account. You are spending your own money that you already have.

-

Spending Limit: You are limited to the funds available in your checking account (unless you have an overdraft protection service, which essentially turns your debit card into a credit tool, often with high fees – more on this later!).

-

Debt Risk: Because you're spending your own money, you generally cannot go into debt by using a debit card, assuming you stay within your available balance.

-

Credit Building: Traditional debit card usage does not help build your credit score, as you are not borrowing money.

-

Examples: Using it to pay for groceries, withdraw cash from an ATM, or pay your monthly utility bill directly from your bank account.

Credit Card: Borrowed Money, a Line of Credit

A credit card, on the other hand, is a loan. When you use a credit card:

-

Source of Funds: You are borrowing money from the credit card issuer (typically a bank or financial institution) up to a pre-approved credit limit. The money doesn't come directly from your checking account at the time of purchase.

-

Spending Limit: You can spend up to your assigned credit limit, regardless of how much cash you currently have in your bank account.

-

Debt Risk: If you don't pay off your full credit card balance by the due date each month, you will be charged interest on the outstanding amount, leading to debt. This is why how to avoid credit card debt is a crucial consideration.

-

Credit Building: Responsible use of a credit card (making on-time payments and keeping balances low) is a primary way to build a positive credit history and improve your credit score.

-

Examples: Using it to pay for a large purchase you want to pay off over time, booking a hotel or rental car (where holds are common), or simply for everyday spending to earn rewards or build credit.

In essence, a debit card is like using digital cash from your wallet, whereas a credit card is like taking a small, short-term loan that you promise to repay. This fundamental difference between credit and debit card impacts everything from fraud protection to rewards and your long-term financial health.

2. Which is safer to use: credit card or debit card?

When it comes to the crucial question of which is safer to use: credit card or debit card, especially in an age of increasing digital transactions and data breaches, credit cards generally offer superior protection. While both have security features, the legal frameworks and operational mechanisms behind them make a significant difference when fraud occurs. This is a key aspect of fraud protection credit card vs debit card.

Here's a breakdown:

Credit Card Safety (Generally Superior):

-

Fraud Liability: Under the Fair Credit Billing Act (FCBA), your maximum liability for unauthorized credit card charges is typically $50, even if your card is stolen or lost. However, most major credit card issuers offer "zero liability" policies, meaning you're not responsible for any fraudulent charges, provided you report them promptly.

-

How it Works: When fraudulent activity occurs on a credit card, you are not out of your own money. The bank's money is at stake. The fraudulent charges appear on your statement, you dispute them, and the bank investigates. During the investigation, you usually don't have to pay for those disputed charges, and once confirmed as fraud, they are removed from your bill. Your personal funds remain untouched.

-

-

Dispute Resolution: Credit card companies generally have robust dispute resolution processes. If you have an issue with a purchase (e.g., you didn't receive the item, or it was not as described), you can dispute the charge with your credit card company, and they will often mediate with the merchant or issue a temporary credit while investigating. This is a powerful consumer protection feature.

-

Holds on Funds: When a merchant places a "hold" on your card (e.g., for a hotel reservation or car rental), it affects your available credit limit, not your actual bank balance. This means your personal funds are not tied up.

-

Less Direct Access to Your Bank Account: Since a credit card is a line of credit and not directly linked to your checking account, a breach of your credit card information doesn't give fraudsters direct access to your primary bank funds.

Debit Card Safety (More Vulnerable):

-

Fraud Liability (Less Favorable): Under the Electronic Funds Transfer Act (EFTA), your liability for fraudulent debit card transactions can be significantly higher if not reported quickly:

-

Within 2 business days: Maximum liability is $50.

-

After 2 business days but within 60 calendar days: Liability can jump to $500.

-

After 60 calendar days: You could be liable for all fraudulent charges.

-

How it Works: When fraudulent activity occurs on a debit card, the money is taken directly from your bank account. This can lead to immediate financial hardship, potentially causing other legitimate transactions to bounce, leading to overdraft fees or non-sufficient funds (NSF) fees. While your bank will typically investigate and eventually reimburse you, it can take days or even weeks for the funds to be returned, leaving you without access to your money.

-

-

Direct Access to Your Bank Account: This is the biggest vulnerability. If a fraudster gains access to your debit card number and PIN (or even just the card number for online purchases), they have direct access to your checking account. This can empty your account, cause overdrafts, and disrupt your ability to pay bills or access necessary funds.

-

Fewer Dispute Protections: While banks do investigate debit card disputes, the process can be slower, and you might have less leverage compared to a credit card dispute.

-

Holds on Funds: When a merchant places a hold on a debit card (common with gas stations, hotels, or rental cars), that specific amount is temporarily unavailable in your checking account, potentially impacting your ability to pay other bills or make purchases.

Conclusion:

So, are credit cards more secure than debit cards? Generally, yes, especially when it comes to fraudulent transactions and the speed of getting your money back. For online purchases, and especially for large transactions or when holds are involved, using a credit card is often the safer bet. While debit cards offer the comfort of spending only what you have, that advantage comes with a higher risk of direct financial disruption in the event of fraud.

3. Can you build credit with a debit card?

This is a common misconception, so let's clear it up directly: Can you build credit with a debit card? The straightforward answer for traditional debit cards is no.

Here's why:

-

Credit Building Requires Borrowing: Building a credit score is fundamentally about demonstrating your ability to borrow money and repay it responsibly. When you use a debit card, you are not borrowing money; you are spending your own money directly from your bank account. Since there's no loan involved, there's no credit relationship to report to the credit bureaus (Experian, Equifax, TransUnion).

-

No Reporting to Credit Bureaus: Credit card companies and lenders report your payment history, credit utilization, length of credit history, and other factors to these credit bureaus. This information is then used to calculate your credit score. Because debit card transactions are simply transfers of your own funds, they are not reported to credit bureaus, and therefore, they do not contribute to your credit score.

What Does Affect Your Credit Score?

Your credit score is built on your history of managing various forms of credit, such as:

-

Credit Cards: Making on-time payments, keeping your credit utilization low (the amount you owe compared to your credit limit), and having a longer history with open accounts. This directly answers does using a credit card help your credit score? (Yes, when used responsibly!)

-

Loans: Mortgages, auto loans, student loans, and personal loans.

-

Lines of Credit: Home equity lines of credit (HELOCs), personal lines of credit.

Are There Exceptions or Alternatives?

While traditional debit cards don't build credit, a few newer, less common products aim to bridge this gap:

-

Secured Credit Cards: These are credit cards, but they require a cash deposit that serves as your credit limit. They are designed for people with no credit or bad credit to build a positive history. Your responsible use is reported to credit bureaus.

-

Credit-Builder Loans: These are small loans where the money is held in a savings account while you make payments. Once the loan is paid off, you get access to the money, and your on-time payments are reported to credit bureaus.

-

Certain Fintech Products: Some innovative financial technology companies are experimenting with "credit-building debit cards" or services that track your rent and utility payments (which are not traditionally reported) and report them to credit bureaus. However, these are not widespread and may not impact all credit scoring models.

The Bottom Line:

If your goal is to build or improve your credit score, a standard debit card is not the tool for the job. You need to engage in borrowing (like a credit card or loan) and demonstrate responsible repayment. While debit card pros and cons include preventing debt, a significant "con" is their inability to help you build a credit history, which is essential for future financial milestones like buying a home or a car, or even getting certain jobs or apartments.

4. Is it better to use a credit card or debit card for online shopping?

When it comes to the digital realm of online shopping, the question is it better to use a credit card or debit card for online shopping? leans heavily in favor of credit cards due to their superior fraud protection and consumer safeguards. This is a critical consideration for credit vs debit for online purchases.

Here's why credit cards often win for online transactions:

-

Superior Fraud Protection (The #1 Reason):

-

Credit Card: As discussed, credit cards generally offer "zero liability" for fraudulent charges. If your credit card number is stolen and used online, the fraudulent charges appear on the card issuer's bill, not directly on your bank account. You dispute the charge, and the bank removes it. Your actual cash funds remain untouched and accessible.

-

Debit Card: If your debit card number is compromised and used for online fraud, the money is immediately drained from your checking account. While banks typically reimburse you, it can take days or even weeks for the funds to be returned. This can lead to a domino effect: legitimate bills might bounce, checks might be returned, and you could face overdraft fees or find yourself unable to access funds for essential living expenses. This is a huge distinction in fraud protection credit card vs debit card.

-

-

Dispute Resolution and Consumer Protections:

-

Credit Card: Credit card companies offer strong consumer protections. If you buy something online and it's not delivered, is damaged, or is significantly different from what was advertised, you can often dispute the charge with your credit card company. They act as an intermediary and can help you get your money back, even if the merchant is uncooperative.

-

Debit Card: While you can dispute debit card charges with your bank, the process is often less robust, and you may have fewer legal protections compared to credit cards, especially for merchandise disputes. You might have to deal with the merchant directly, which can be challenging.

-

-

No Direct Bank Account Access:

-

Credit Card: Since your credit card isn't directly linked to your checking account, a data breach affecting an online merchant (or your credit card information) doesn't give fraudsters immediate access to all your bank funds. They only have access to your credit line.

-

Debit Card: A compromised debit card can be a direct pipeline to your entire bank balance, making it a higher risk for large-scale financial disruption.

-

-

Security Layers:

-

Both credit and debit cards use encryption and other security protocols for online transactions. However, many credit card companies offer additional layers like virtual card numbers, which provide a single-use or temporary card number for online purchases, further isolating your actual card details from merchants.

-

-

Rewards and Benefits:

-

Credit Card: Many credit cards offer rewards programs (cashback, travel points, airline miles) for online purchases, effectively giving you a small percentage back on your spending. They might also offer extended warranties, purchase protection, or return protection.

-

Debit Card: While some debit cards now offer limited rewards, they are generally far less generous than credit card rewards programs.

-

When a Debit Card Might Be Considered (with Caution):

-

Strict Budgeting: If you have severe spending discipline issues or want to absolutely ensure you don't overspend, a debit card forces you to use only the money you have. This aligns with best card for budgeting if you struggle with credit card temptation.

-

Small, Insignificant Purchases: For very minor online purchases where the risk of significant loss from fraud is low, a debit card might be acceptable if you prefer to avoid credit.

The Smart Choice:

For the vast majority of online shopping, a credit card is the smarter and safer choice. The enhanced fraud protection credit card vs debit card offers, coupled with consumer dispute rights and potential rewards, far outweigh the perceived simplicity of a debit card. If you're concerned about how to avoid credit card debt while using a credit card online, simply pay off your balance in full immediately after your purchase posts, or at the end of each billing cycle.

5. Are credit cards more secure than debit cards?

To reiterate and expand on a crucial point, are credit cards more secure than debit cards? The answer is a resounding yes, particularly when it comes to protecting your money and your financial stability in the event of fraud or disputes. This enhanced security is one of the most significant credit card advantages and disadvantages (advantage for credit cards, disadvantage for debit cards).

Let's delve deeper into why credit cards offer superior security:

-

Who Loses the Money First?

-

Credit Card: When a fraudulent charge occurs on your credit card, the money lost initially belongs to the credit card issuer, not you. You're not immediately out of pocket. This means your checking account balance remains untouched, and your ability to pay rent, groceries, or other bills isn't directly impacted. The burden of investigation and recovery falls primarily on the credit card company.

-

Debit Card: With a fraudulent debit card transaction, your actual cash funds are immediately removed from your bank account. This can cause immediate financial distress, leading to bounced checks, declined legitimate transactions, and potentially overdraft fees. While your bank will likely investigate and reimburse you, the process can take days or weeks, leaving you in a precarious financial position during that time. This is the fundamental difference in fraud protection credit card vs debit card.

-

-

Legal Protections (FCBA vs. EFTA):

-

Credit Cards (Fair Credit Billing Act - FCBA): The FCBA provides robust protection. Your maximum liability for unauthorized charges is limited to $50, and often zero if reported promptly. This protection extends to billing errors and issues with goods or services purchased.

-

Debit Cards (Electronic Funds Transfer Act - EFTA): While the EFTA offers some protection for debit cards, it's not as strong or immediate as the FCBA for credit cards. As mentioned, your liability can escalate significantly if fraud isn't reported very quickly (within two business days). The focus of EFTA is more on unauthorized electronic fund transfers, not necessarily disputes over merchandise.

-

-

Impact of Holds:

-

Credit Cards: When a hotel, rental car company, or gas station places a "hold" on your card (to ensure you have sufficient funds or to cover potential damages), it reduces your available credit limit. Your cash in your bank account is untouched.

-

Debit Cards: A hold on a debit card freezes actual funds in your checking account. This means that money is inaccessible to you, potentially leading to a low or negative balance and causing legitimate transactions to be declined, triggering overdraft fees.

-

-

No Direct Link to Core Funds:

-

The separation of your credit card account from your primary checking and savings accounts provides an additional layer of security. If your credit card information is compromised, criminals do not automatically gain access to your entire financial livelihood. This contrasts sharply with debit cards, where compromised information is a direct conduit to your liquid cash.

-

-

Additional Credit Card Security Features:

-

Many credit card issuers offer advanced fraud monitoring, real-time alerts for suspicious activity, and the ability to freeze your card instantly via a mobile app. Some even provide virtual card numbers for one-time online use, adding another layer of anonymity and protection.

-

In summary, while banks have improved debit card pros and cons by enhancing fraud monitoring and zero-liability policies for debit cards, the inherent nature of a credit account (borrowed money) versus a debit account (your money) makes credit cards generally more secure in the event of fraud. When asked which is safer: credit or debit card, the answer for almost all scenarios involving potential fraud is credit.

6. What are the pros and cons of using a credit card?

Understanding the credit card advantages and disadvantages is essential for responsible financial management. They are powerful tools, but like any powerful tool, they can be harmful if misused.

Pros of Using a Credit Card:

-

Credit Building: This is arguably the most significant long-term advantage. Does using a credit card help your credit score? Absolutely, when used responsibly. Consistently making on-time payments and keeping your credit utilization low (below 30% of your credit limit) builds a positive credit history, which is vital for getting loans (mortgage, auto), renting apartments, and even some jobs.

-

Fraud Protection: As discussed extensively, credit cards offer superior fraud protection credit card vs debit card. You're typically not liable for fraudulent charges, and your own money isn't immediately at risk.

-

Rewards and Benefits: Many credit cards offer valuable rewards programs, including:

-

Cashback: A percentage of your spending returned to you.

-

Travel Points/Miles: Can be redeemed for flights, hotels, or other travel perks. This directly relates to travel benefits credit card vs debit card.

-

Sign-up Bonuses: Large bonuses for meeting initial spending requirements.

-

Additional Perks: Extended warranties, purchase protection, return protection, rental car insurance, and concierge services.

-

-

Emergency Fund Supplement: While not a replacement for an emergency fund, a credit card can provide a crucial safety net for unexpected expenses, especially if your emergency fund is low or for very large, immediate needs, offering flexibility that a debit card cannot.

-

Convenience and Acceptance: Widely accepted globally, making them convenient for transactions both online and in-store. Often required for large purchases or reservations like rental cars and hotel bookings (due to holds on funds).

-

Interest-Free Grace Period: If you pay your balance in full by the due date each month, you generally won't be charged interest on your purchases. This means you can essentially borrow money for free for a short period.

-

Detailed Spending Records: Credit card statements provide an excellent record of your spending, which can be useful for budgeting and tracking expenses.

Cons of Using a Credit Card:

-

Risk of Debt and Interest: This is the biggest drawback. If you don't pay your balance in full each month, you'll incur high interest charges, which can quickly spiral into significant debt. This is why learning how to avoid credit card debt is paramount.

-

Temptation to Overspend: The ease of use and the fact that you're not seeing money immediately leave your bank account can lead to overspending and buying things you can't truly afford.

-

Fees: While many cards have no annual fee, some do. Other common fees include late payment fees, balance transfer fees, cash advance fees (which come with immediate interest), and foreign transaction fees (an important point for travel benefits credit card vs debit card).

-

Negative Impact on Credit Score: While credit cards can build credit, they can also damage it if misused. Late payments, high credit utilization, and too many new accounts can significantly lower your score.

-

Complexity: Understanding interest rates, billing cycles, grace periods, rewards programs, and various fees can be complex for beginners.

-

Minimum Payments: Making only the minimum payment keeps you in debt longer and dramatically increases the total interest you pay.

In summary, credit cards are powerful financial tools with significant benefits, especially for building credit and offering fraud protection. However, they demand discipline and careful management to avoid falling into debt and incurring high fees. For someone asking is a credit card better than a debit card? the answer depends entirely on their ability to use credit using credit card responsibly.

7. Why should I use a debit card instead of a credit card?

While credit cards offer significant advantages in terms of fraud protection and credit building, there are compelling reasons why should I use a debit card instead of a credit card in certain situations. The primary appeal of a debit card lies in its direct connection to your money and its inherent simplicity, making it a strong contender for best card for budgeting.

Here are the key reasons to choose a debit card:

-

Debt Prevention (Spending Only What You Have):

-

Core Benefit: The most significant advantage of a debit card is that it directly debits funds from your bank account. This means you can only spend the money you actually possess. There's no borrowing involved, and thus, no risk of incurring interest charges or accumulating debt.

-

Ideal for: Individuals who struggle with overspending, those who are just learning to manage money (like students, addressed in student credit card vs debit card), or anyone committed to a strict budget. It acts as an immediate spending governor.

-

-

Simplicity and Predictability:

-

Straightforward Transactions: There are no complex billing cycles, grace periods, interest rates, or minimum payments to track. The money simply leaves your account.

-

Easier Budgeting: For many, the immediate deduction of funds makes it easier to keep track of their spending and stick to a budget. You can see your bank balance decrease in real-time, offering a clear picture of your available funds. This truly makes it a best card for budgeting.

-

-

ATM Access:

-

Cash Withdrawals: Debit cards are the primary tool for withdrawing cash from ATMs from your checking account. While credit cards offer cash advances, these are almost always accompanied by high fees and immediate interest charges, making them a very expensive way to get cash.

-

-

No Annual Fees or Interest Charges:

-

Most standard debit cards come with no annual fees. Since you're not borrowing money, there are no interest charges on purchases. This contrasts with some credit cards that charge annual fees or high interest if balances are carried.

-

-

Lower Barrier to Entry:

-

Debit cards are typically issued automatically when you open a checking account. There are no credit checks involved, making them accessible to anyone, regardless of their credit history or lack thereof. This makes them ideal for individuals without established credit, such as younger adults or new immigrants, directly relevant to student credit card vs debit card.

-

-

Avoiding Credit Card Temptation:

-

For those who know they might be tempted to overspend or fall into debt with a credit card, sticking to a debit card can be a disciplined choice to protect their financial health.

-

When Debit Cards are a Strong Choice:

-

Daily Spending: For everyday purchases like groceries, gas, or coffee, a debit card can be a practical choice, especially if you prioritize avoiding debt.

-

ATM Withdrawals: This is their undeniable strength.

-

Budget Adherence: If strict budgeting is your goal and you want to ensure you never spend more than you have.

While debit cards lack the fraud protection and credit-building potential of credit cards, their simplicity and debt-prevention capabilities make them an excellent choice for certain financial habits and situations. The choice between credit card vs debit card often comes down to personal discipline and financial goals.

8. Does using a credit card help your credit score?

The direct answer to does using a credit card help your credit score? is a resounding yes, absolutely – provided you use it responsibly. In fact, a credit card is one of the most effective and common tools for building and improving your credit score. This is a significant advantage in the credit card advantages and disadvantages discussion.

Here's how responsible credit card use positively impacts your credit score:

-

Payment History (The Biggest Factor):

-

Positive Impact: Your payment history accounts for approximately 35% of your FICO score (the most widely used credit scoring model). Every time you make a payment on your credit card by the due date, it's a positive mark on your credit report.

-

Negative Impact: Conversely, late payments (typically 30 days or more past due) can severely damage your credit score and stay on your report for up to seven years.

-

How to Optimize: Always pay your credit card bill on time, every single month. Consider setting up automatic payments to ensure you never miss a due date.

-

-

Credit Utilization (Amount Owed):

-

Positive Impact: This factor accounts for about 30% of your FICO score. It's the ratio of your total credit card balances to your total credit limits. Lenders prefer to see low utilization, ideally below 30%. The lower, the better, with the best scores often associated with utilization under 10%.

-

How to Optimize: Even if you can't pay your full balance, try to pay it down as much as possible before your statement closing date. For optimal credit building, pay your balance in full every month. This practice is key to using credit card responsibly.

-

-

Length of Credit History:

-

Positive Impact: This factor (around 15% of your score) looks at how long your credit accounts have been open and the average age of your accounts. The longer you've had credit, and the older your oldest account is, the better.

-

How to Optimize: Keep your oldest credit card accounts open, even if you don't use them frequently, as long as they don't have annual fees. Your first credit card can become a cornerstone of a long credit history.

-

-

Credit Mix:

-

Positive Impact: (Around 10% of your score) Lenders like to see that you can manage different types of credit (e.g., revolving credit like credit cards and installment loans like mortgages or auto loans). Having a mix can positively influence your score.

-

How to Optimize: As your financial life progresses, gradually acquire different types of credit, but only what you need and can responsibly manage.

-

-

New Credit:

-

Negative Impact (Temporary): (Around 10% of your score) Opening too many new credit accounts in a short period can temporarily lower your score because it suggests you might be taking on too much debt.

-

How to Optimize: Apply for new credit only when necessary and space out applications.

-

Why Debit Cards Don't Build Credit:

As established in "Can you build credit with a debit card?", debit cards are not reported to credit bureaus because they don't involve borrowing. Therefore, their usage has no impact, positive or negative, on your credit score. This is a fundamental difference between credit and debit card in terms of credit impact.

The Bottom Line:

If you're committed to building credit score with a credit card, it's a powerful and effective tool. By consistently paying your bills on time and keeping your balances low, you'll establish a strong credit history that can open doors to better interest rates on loans, easier approvals for housing, and overall greater financial flexibility. It's an indispensable component of sound financial planning with credit and debit cards.

9. Can using a debit card lead to overdraft fees?

Yes, absolutely. While a major debit card pros and cons point is that you can only spend what you have, a common pitfall is that can using a debit card lead to overdraft fees? The answer is a definite yes, and it's a significant financial risk to be aware of.

Here's how it happens and what you need to know:

-

What is an Overdraft?

-

An overdraft occurs when you make a transaction for more money than you have available in your checking account.

-

When this happens, your bank has a choice:

-

They can decline the transaction.

-

They can pay the transaction, even though you don't have enough funds, effectively extending you a very short-term, high-cost loan. When they do this, they typically charge you an overdraft fee.

-

-

-

How Debit Cards Cause Overdrafts:

-

Single Large Purchase: You swipe your debit card for a $100 purchase, but you only have $50 in your account. If your bank's overdraft policy allows it, they might cover the $50 deficit, and then charge you an overdraft fee (often around $25-$35 per transaction).

-

Multiple Small Purchases: You make several small purchases throughout the day, not realizing your balance is low. Each transaction that pushes you into the negative (or further negative) can trigger a separate overdraft fee. These can add up incredibly quickly.

-

Holds on Funds: Sometimes, merchants (like gas stations or hotels) place a temporary "hold" on your debit card for a certain amount. If this hold, combined with other spending, causes your balance to dip too low, subsequent transactions could trigger overdrafts, even if the hold amount is later adjusted.

-

Pending Transactions: A common scenario is when you have pending transactions (e.g., an online purchase that hasn't officially posted yet). You might see a higher available balance than what's truly there, leading you to spend money that isn't actually available.

-

-

Overdraft Protection "Opt-In":

-

For one-time debit card purchases and ATM withdrawals, federal regulations (in the U.S., for example) require banks to get your "opt-in" consent before they can charge you an overdraft fee. If you don't opt-in, the bank must decline the transaction if it would overdraw your account, and you won't be charged a fee for that specific transaction (though the merchant might charge you a "returned item" fee).

-

However, for checks and recurring electronic payments (like gym memberships or streaming services), banks can still charge overdraft fees even if you haven't opted in for debit card overdraft protection.

-

-

Consequences of Overdrafts:

-

High Fees: As mentioned, overdraft fees are expensive, typically $25-$35 per instance.

-

Cascading Effect: One overdraft can lead to several, as your low balance continues to trigger fees with subsequent transactions.

-

Impact on Financial Standing: While a single overdraft won't directly hurt your credit score (as debit card transactions aren't reported to credit bureaus), consistently overdrawing your account can lead to your bank closing your account, making it difficult to open a new one elsewhere. If the bank sends your overdrawn balance to collections, that could negatively impact your credit.

-

How to Avoid Overdraft Fees with a Debit Card:

-

Track Your Spending Diligently: Keep a close eye on your bank balance. Use online banking or mobile apps regularly.

-

Opt-Out of Overdraft Protection: For debit card transactions, opt out of overdraft protection. This means your card will be declined if you don't have enough funds, but you'll avoid the fee.

-

Link to Savings/Line of Credit: Set up overdraft protection that links your checking account to a savings account or a line of credit. This way, if you overdraw, funds are transferred from your linked account to cover the deficit (though there might be a small transfer fee, it's usually much less than an overdraft fee).

-

Maintain a Buffer: Always keep a small buffer amount (e.g., $100-$200) in your checking account that you consider "off-limits" for spending.

-

Use a Credit Card for Buffer: For situations where a hold might be placed (hotels, rental cars, gas at the pump), consider using a credit card to avoid tying up your checking account funds, tying into the credit vs debit for online purchases and general safety discussions.

In conclusion, while debit cards are great for preventing debt from borrowing, they do carry a significant risk of overdraft fees if you're not meticulous with your account balance. This is an important debit card pros and cons consideration that highlights the nuances of financial planning with credit and debit cards.

10. Which card is best for travel: credit or debit?

When planning a trip, the question which card is best for travel: credit or debit? often comes up. For most international and even significant domestic travel, the resounding answer from financial experts and seasoned travelers is almost always the credit card. Its superior security, benefits, and flexibility make it the smarter choice for travel benefits credit card vs debit card.

Here's a breakdown of why credit cards typically outperform debit cards for travel:

-

Superior Fraud Protection (Crucial for Travel):

-

Credit Card: If your credit card is compromised while traveling (a common occurrence), fraudulent charges don't directly drain your bank account. You dispute the charges, and the credit card company deals with the fraud, meaning your spending money for the rest of your trip remains untouched. This is paramount for fraud protection credit card vs debit card when abroad.

-

Debit Card: If your debit card is compromised, the fraudulent transactions come directly from your checking account. This can leave you stranded without cash for essentials, potentially leading to bounced payments and stress while you wait for your bank to investigate and return your funds.

-

-

Holds on Funds (Hotels, Rental Cars):

-

Credit Card: Hotels and car rental agencies frequently place a "hold" on your card for incidentals or potential damages. With a credit card, this hold reduces your available credit limit, but it doesn't tie up your actual cash funds.

-

Debit Card: A hold on a debit card freezes an equivalent amount of your own money in your checking account. This can significantly reduce your available cash, potentially causing other legitimate transactions to be declined or leading to overdraft fees. Many rental car companies even outright refuse debit cards for this reason or require a significant cash deposit.

-

-

Emergency Funds and Flexibility:

-

Credit Card: In an emergency (medical, unexpected expense, missed flight), a credit card provides an immediate line of credit that a debit card cannot. It offers crucial financial flexibility when you might not have access to sufficient cash.

-

Debit Card: If you run out of funds in your checking account, your debit card becomes useless, leaving you in a difficult spot.

-

-

Travel Rewards and Benefits:

-

Credit Card: Many travel-focused credit cards offer incredible perks:

-

Travel Miles/Points: Earn points on all spending that can be redeemed for flights, hotel stays, or other travel expenses.

-

Travel Insurance: Coverage for trip cancellation/interruption, baggage delay/loss, and even emergency medical assistance.

-

Rental Car Insurance: Often covers collision damage waiver, saving you from expensive daily rental agency fees.

-

No Foreign Transaction Fees: Many credit cards waive these fees (typically 1-3% of each transaction), which can add up significantly on international trips. This is a huge travel benefits credit card vs debit card differentiator.

-

Airport Lounge Access, Upgrades, Concierge Services: Higher-tier cards offer luxurious perks.

-

-

Debit Card: While some debit cards offer limited rewards or no foreign transaction fees, they are typically nowhere near as comprehensive or lucrative as credit card programs.

-

-

Building Credit While Traveling:

-

Credit Card: Every responsible purchase you make and pay off on time while traveling contributes positively to your credit score, especially if it's a card you use regularly.

-

Debit Card: Has no impact on your credit score.

-

When a Debit Card Still Has a Place in Travel (as a secondary tool):

-

Cash Withdrawals: Your debit card is ideal for withdrawing local currency from ATMs. Look for ATMs associated with your bank's network (or partner networks) to avoid fees. Carry a small amount of cash for places that don't accept cards.

-

Budget Control: If you want to strictly limit spending in certain situations, a debit card ensures you don't go over your budgeted cash amount.

-

Backup Card: Always carry both a credit and a debit card (and perhaps some cash) from different accounts, and store them in separate, secure places. If one is lost or stolen, you have a backup.

The Smart Travel Strategy:

For travel, especially internationally, a credit card is usually the smarter primary payment method due to its unparalleled security, consumer protection, and potential for valuable travel rewards. Use your debit card primarily for cash withdrawals at ATMs, and always have it as a backup. This balanced approach ensures you're protected, flexible, and maximizing your travel experience.

Credit Card vs. Debit Card: The Smart Spender's Playbook

Phew! We've taken a deep dive into the world of plastic, comparing the mighty credit card vs debit card. Hopefully, you're no longer staring blankly at your wallet, but rather with a newfound sense of clarity and purpose.

The big takeaway here isn't that one card is inherently "better" than the other for everything. Instead, it's about understanding the unique strengths and weaknesses of each, and using them strategically. Your debit card, linked directly to your hard-earned cash, is your ultimate tool for staying on budget and avoiding debt – a true best card for budgeting. It's pure, unadulterated "pay-as-you-go" simplicity.

But don't underestimate the power of the credit card. When used using credit card responsibly, it transforms from a potential debt trap into a powerful ally. It's your shield against fraud (remember how fraud protection credit card vs debit card heavily favors credit?), your ladder for building credit score with a credit card that opens doors to future financial goals, and your ticket to exciting travel benefits credit card vs debit card and rewards.

So, the next time you're about to make a purchase, take a moment to consider the context. Is it a small, everyday expense where you want strict budget control? Debit might be your go-to. Is it a large online purchase, a hotel booking, or anything that carries a higher risk or potential reward? Swipe that credit card, then pay it off in full!

By mastering the difference between credit and debit card and incorporating both wisely into your financial planning with credit and debit cards, you're not just making transactions. You're making smart financial decisions that pave the way for a more secure and rewarding future. Go forth and swipe smartly!

Maybe you are interested:

Passive Income vs Active Income: Which One Builds Long-Term Wealth Smarter?

Emergency Fund vs Insurance: What Should You Prioritize First for Financial Security?

More Like This

How to Improve Your Life: A Complete Guide to Personal Growth

by Emily Cooper

Why is sleep important? What do you need to know about sleep?

by Emily Cooper